Health insurance can often feel complicated, especially for first-time buyers who encounter unfamiliar terminology. However, understanding basic health insurance terms is essential for making smart healthcare and financial decisions. Misinterpreting policy language can lead to unexpected medical bills, denied claims, or choosing the wrong plan.

This SEO-optimized guide explains the most important health insurance terminology in simple language so you can confidently compare plans and maximize your coverage in 2026.

Why Understanding Health Insurance Terms Matters

Learning key health insurance vocabulary helps you:

- Compare health insurance plans accurately

- Avoid hidden out-of-pocket costs

- Maximize policy benefits

- Reduce the risk of claim rejection

- Select cost-effective medical coverage

Because insurance policies are legal contracts, knowing these terms gives you a major financial advantage.

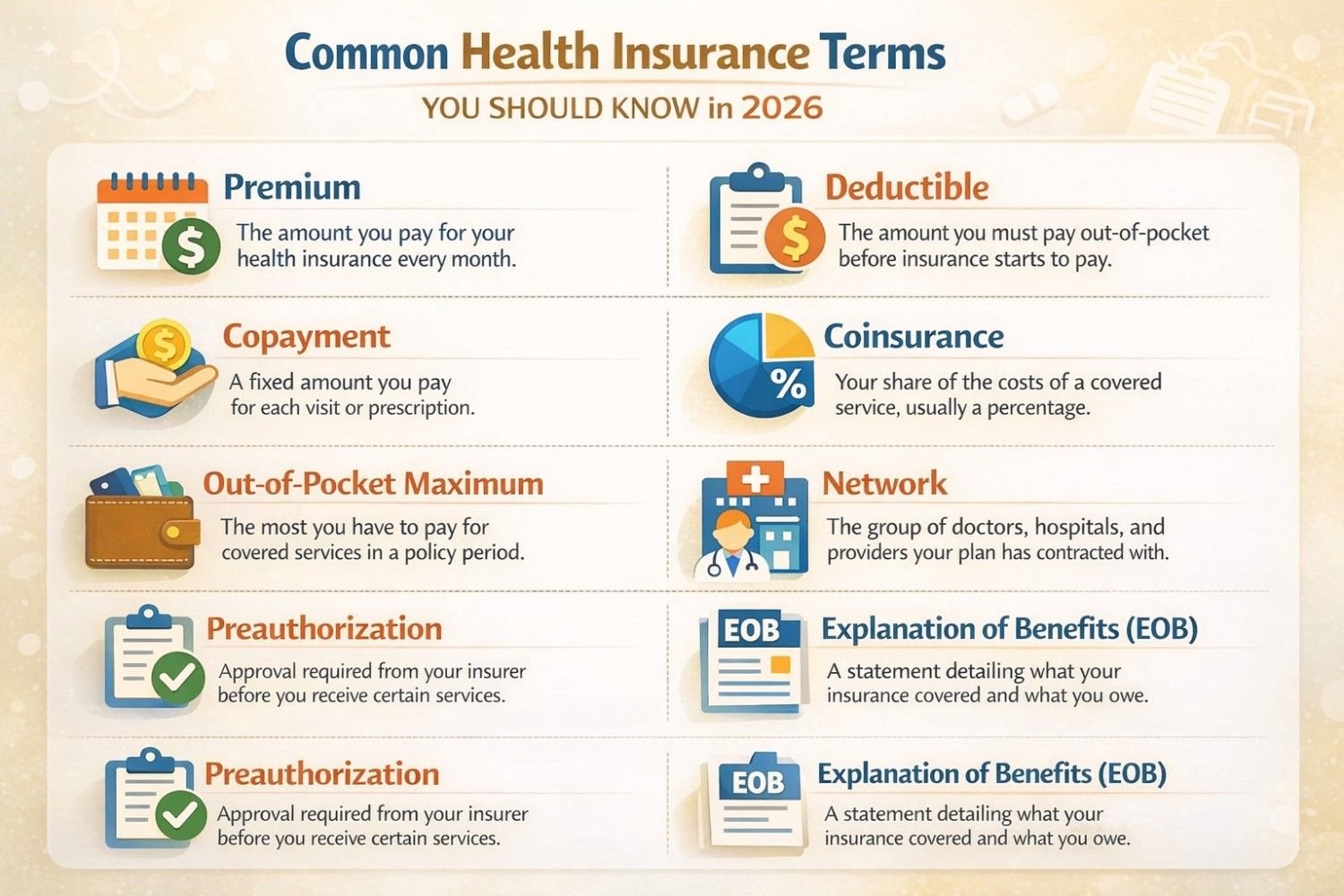

Premium

The health insurance premium is the amount you pay regularly—monthly, quarterly, or annually—to keep your policy active.

- Must be paid even if you don’t use medical services

- Lower premiums usually mean higher deductibles

- Higher premiums often provide broader coverage

Deductible

A health insurance deductible is the amount you must pay out of pocket before your insurer starts covering eligible medical expenses.

| Deductible Type | Meaning | Best For |

|---|---|---|

| Low Deductible | Higher premium, lower upfront costs | Families and chronic patients |

| High Deductible | Lower premium, higher upfront costs | Young and healthy individuals |

Co-Pay (Copayment)

A copay is a fixed fee you pay for specific healthcare services.

Examples:

- $30 primary care visit

- $50 specialist consultation

- $10–$20 generic prescription

Copays help make routine healthcare costs predictable.

Co-Insurance

Co-insurance is the percentage of medical costs you share with your insurer after meeting your deductible.

Example: If your plan is 80/20, the insurer pays 80% and you pay 20% until you reach your out-of-pocket maximum.

Out-of-Pocket Maximum

The out-of-pocket maximum is the highest amount you must pay in a policy year for covered services.

- After reaching this limit, insurance pays 100% of eligible costs

- Provides protection against catastrophic medical expenses

Provider Network

A health insurance network is the group of doctors, hospitals, and clinics partnered with your insurer.

- In-network: Lower costs

- Out-of-network: Higher costs or no coverage

Always check network coverage before choosing a plan.

HMO vs PPO vs EPO vs POS Plans

- HMO (Health Maintenance Organization): Lower cost, limited flexibility

- PPO (Preferred Provider Organization): Higher cost, more provider freedom

- EPO (Exclusive Provider Organization): No out-of-network coverage

- POS (Point of Service): Hybrid of HMO and PPO

Pre-Existing Condition

A pre-existing condition is any medical issue you had before purchasing insurance, such as diabetes, asthma, or heart disease.

Important: Always disclose these conditions honestly to avoid claim denial.

Exclusions

Policy exclusions are services or treatments your insurance does not cover. Common exclusions include:

- Cosmetic procedures

- Experimental treatments

- Non-prescribed therapies

Waiting Period

The waiting period is the time you must wait before certain benefits become active.

- Maternity coverage: typically 9–12 months

- Pre-existing conditions: up to 24 months

Claim

A health insurance claim is a formal request to your insurer for payment of medical expenses.

Types of claims:

- Cashless claims (direct hospital billing)

- Reimbursement claims

Riders / Add-Ons

Insurance riders are optional benefits that enhance your base policy.

Popular add-ons include:

- Critical illness rider

- Accidental disability cover

- Global emergency coverage

Policy Term

The policy term is the duration your health insurance remains active—typically one year. Always renew on time to avoid coverage gaps.

Grace Period

The grace period is extra time allowed after your premium due date. Missing this window can result in policy cancellation.

Tax Benefits

Many countries offer tax deductions on health insurance premiums, particularly through employer-sponsored plans. These benefits improve the overall value of your policy.

Common Health Insurance Mistakes to Avoid

- Choosing plans based only on low premiums

- Ignoring deductibles and out-of-pocket limits

- Not checking provider networks

- Failing to disclose medical history

Expert Tips for Choosing the Right Health Insurance

- Read policy documents carefully

- Ask insurers detailed questions

- Compare multiple health insurance plans

- Review your coverage every year

Final Thoughts

Understanding common health insurance terms is one of the smartest steps you can take toward better financial and medical protection. In 2026, healthcare costs are too high to rely on guesswork.

The more you understand your policy, the better protected you are. Knowledge isn’t just power—it’s protection.