Despite being one of the most powerful financial protection tools, life insurance is still widely misunderstood. Across Tier-1 countries such as the United States, Canada, the United Kingdom, and Australia, many people delay buying coverage because of persistent myths and outdated advice.

These misconceptions can lead to underinsurance, higher long-term costs, and financial hardship for families. In this SEO-optimized guide, we debunk the most common life insurance myths and reveal the facts every smart policyholder should know.

Why Life Insurance Myths Are Financially Risky

Believing incorrect information about life insurance coverage can create serious long-term consequences, including:

- Buying insufficient coverage

- Overpaying for the wrong policy

- Delaying protection until premiums rise

- Leaving dependents financially exposed

Understanding the truth helps you make confident and cost-effective insurance decisions.

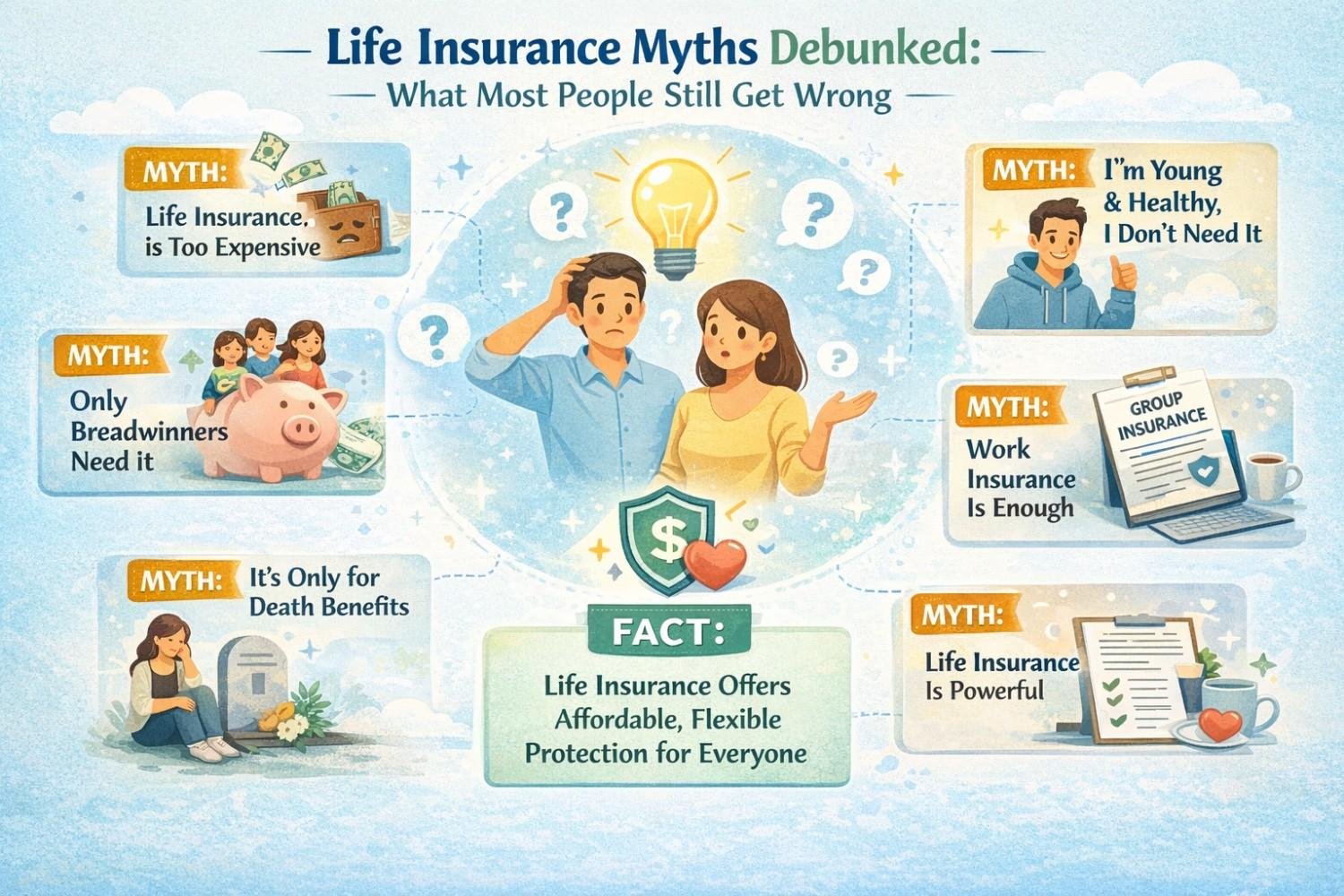

Myth #1: Life Insurance Is Only for Older People

This is one of the most damaging misconceptions. In reality, life insurance premiums are lowest when you are young and healthy.

As age and health risks increase, premiums rise significantly. Locking in a policy early—especially term life insurance—can secure low rates for decades.

Fact: Young professionals, newly married couples, and new parents often benefit the most from early coverage.

Myth #2: Life Insurance Is Too Expensive

Many consumers overestimate the cost of life insurance policies by three to five times. In many Tier-1 markets, basic term coverage can cost less than a daily coffee.

| Age | Coverage Amount | Estimated Monthly Cost |

|---|---|---|

| 30 | $500,000 | $20–$30 |

| 40 | $500,000 | $35–$50 |

| 50 | $500,000 | $70–$100 |

Fact: Life insurance remains one of the most affordable financial protection products available.

Myth #3: Employer Life Insurance Is Enough

Employer-provided coverage typically equals only 1–2 times your annual salary. For most households, this is far below recommended protection levels.

Additionally, workplace coverage usually ends if you change jobs, retire, or are laid off.

Fact: A personal life insurance policy ensures continuous, portable protection.

Myth #4: Stay-At-Home Parents Don’t Need Life Insurance

Non-working spouses provide significant economic value through childcare, household management, and family support.

Replacing these services can cost tens of thousands per year.

Fact: Stay-at-home parents absolutely need life insurance protection.

Myth #5: Single People Don’t Need Life Insurance

Even without dependents, many individuals have financial responsibilities such as:

- Co-signed student loans

- Aging parents

- Business obligations

- Estate planning goals

Fact: Life insurance protects more than just spouses and children.

Myth #6: Life Insurance Only Pays After Death

Many modern permanent life insurance policies include valuable living benefits, such as:

- Cash value accumulation

- Policy loans

- Tax-advantaged growth

- Supplemental retirement income strategies

Fact: Some life insurance policies can support your finances during your lifetime.

Myth #7: Term Life Insurance Is a Waste of Money

Critics often overlook the primary purpose of term life insurance: providing maximum coverage at the lowest cost during high-responsibility years.

Fact: Term policies offer the most cost-efficient protection for income replacement needs.

Myth #8: Whole Life Insurance Is Always a Bad Investment

Whole life insurance is not meant to replace traditional investments—it complements them.

Key benefits include:

- Guaranteed death benefit

- Tax-deferred cash value growth

- Predictable long-term returns

- Estate planning advantages

Fact: Permanent life insurance can play a strategic role in long-term wealth planning.

Myth #9: Only Breadwinners Need Coverage

Every contributing household member has economic value, whether through income generation or essential services.

Fact: A comprehensive family financial plan often includes coverage for multiple household members.

Myth #10: Life Insurance Claims Rarely Get Paid

In most Tier-1 markets, major insurers maintain claim settlement ratios above 95%.

Delays usually occur due to:

- Incomplete documentation

- Policy exclusions

- Non-disclosure at application

Fact: Valid life insurance claims are typically paid promptly.

Why Life Insurance Myths Persist

- Lack of financial literacy

- Complex insurance terminology

- Outdated advice

- Fear-based marketing narratives

How to Make Smarter Life Insurance Decisions

- Evaluate long-term financial obligations

- Compare term vs. permanent life insurance

- Purchase coverage early for lower premiums

- Review policies regularly as life changes

Final Thoughts: Facts Matter More Than Myths

Life insurance myths can quietly undermine your family’s financial security. The reality is clear: modern life insurance is affordable, flexible, and essential for long-term protection.

By separating fact from fiction, you can confidently protect your loved ones, preserve wealth, and build a stronger financial future. Smart financial planning starts with informed decisions—and life insurance remains one of the smartest moves you can make in 2026.